Have you heard that you should “make your money work for you” or “put your money to work”?

Here’s a quick breakdown:

- You probably earn money with a job.

- That money can earn money (interest) through investment accounts and (to a lesser degree) bank accounts.

- And then, if you leave it there, you’ll see the magic of compound interest.

Compound interest 101

Dictionary.com defines compound interest as “interest paid on both the principal and on accrued interest.”

What does it look like?

- You earn money with a job.

- You put that money into a bank account and/or an investment account.

- You are paid interest on the principal (the money you invested).

- Next time, you are paid interest on the money you invested PLUS the interest that was added to the account last time.

Your interest earns interest!

The most common ways to earn interest are through investment accounts or savings accounts. So how different are they?

Let’s say you are going to either save or invest* $300 once per month for 20 years:

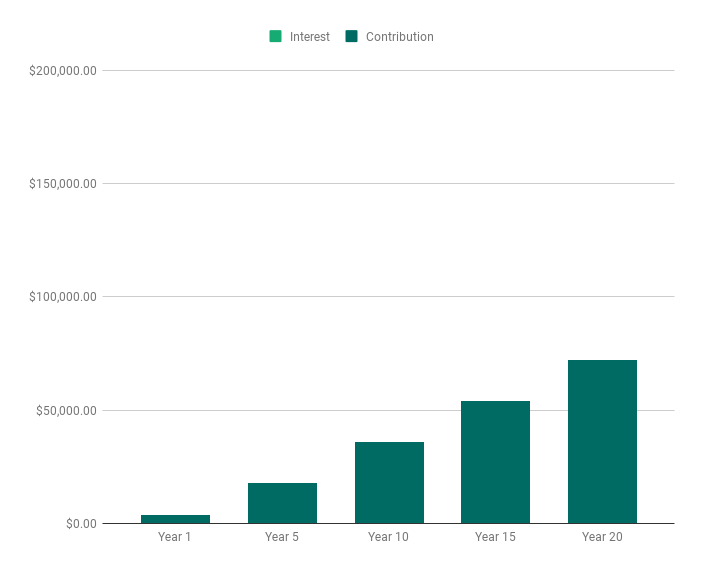

Scenario A: Standard savings account earning 0.01% interest APY

Year 1: $3,600.18

- Your $3,600 contribution = 99.995%

- You earned $0.18 in interest = 0.005%

Year 5: $18,004.50

- Your $18,000 contribution = 99.975%

- You earned $4.50 in interest = 0.025%

Year 10: $36,018

- Your $36,000 contribution = 99.950%

- You earned $18 in interest = 0.050%

Year 15: $54,040.51

- Your $54,000 contribution = 99.925%

- You earned $40.51 in interest = 0.075%

Year 20: $72,072.04

- Your $72,000 contribution = 99.900%

- You earned $72.04 in interest = 0.100%

After 20 years, you’ve earned just $72.04 in interest.

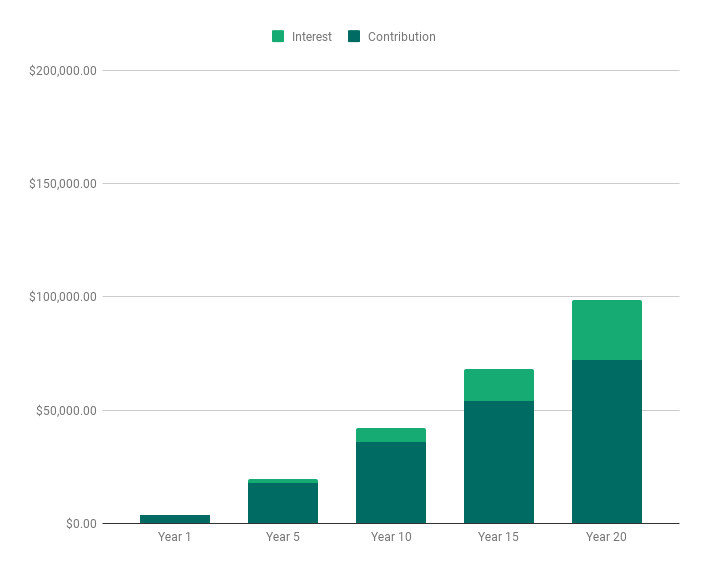

Scenario B: High-yield savings account earning 3% interest APY

Year 1: $3,654.39

- Your $3,600 contribution = 98.5%

- You earned $54.39 in interest = 1.5%

Year 5: $19,419.25

- Your $18,000 contribution = 92.7%

- You earned $1,419.25 in interest = 7.3%

Year 10: $41,981.06

- Your $36,000 contribution = 85.8%

- You earned $5,981.06 in interest = 14.2%

Year 15: $68,193.98

- Your $54,000 contribution = 79.2%

- You earned $14,193.98 in interest = 20.8%

Year 20: $98,648.86

- Your $72,000 contribution = 73.0%

- You earned $26,648.86 in interest = 27.0%

In the very first year, you already earned more interest than you did in 20 years with the standard savings account! After 20 years, you deposited the same $72,000, but you have an extra $26,576.82 to show for it.

Not bad, but are you ready to more-than-triple your interest??

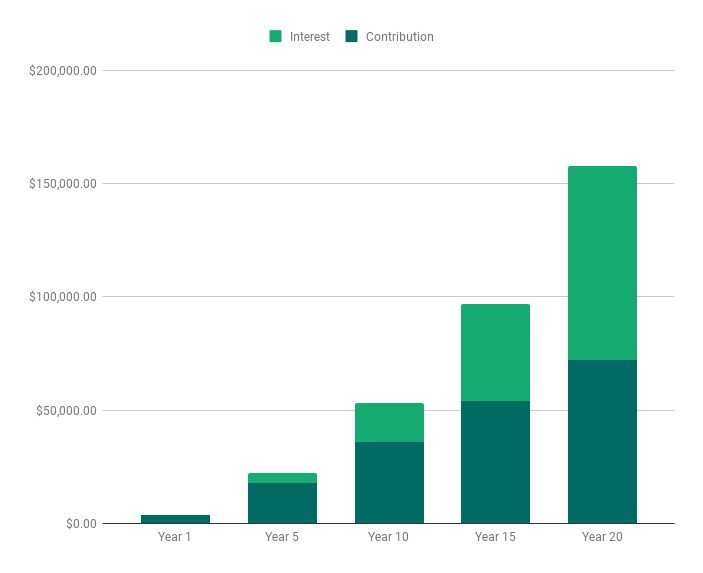

Scenario C: Investment account* earning 7%** interest APY

Year 1: $3,852.00

- Your $3,600 contribution = 93.5%

- You earned $252 in interest = 6.5%

Year 5: $22,151.85

- Your $18,000 contribution = 81.3%

- You earned $4,151.85 in interest = 18.7%

Year 10: $53,220.96

- Your $36,000 contribution = 67.6%

- You earned $17,220.96 in interest = 32.4%

Year 15: $96,796.99

- Your $54,000 contribution = 55.8%

- You earned $42,796.99 in interest = 44.2%

Year 20: $157,914.64

- Your $72,000 contribution = 45.6%

- You earned $85,914.64 in interest = 54.4%

After 20 years, you’ve deposited the same $72,000 but earned $59,265.78 more in interest compared to the high yield savings account scenario. More than half of the money in your account is from accumulated interest!

*When I say “invest” or “investment account,” I’m talking about a retirement account (IRA, 401(k), 403(b), etc.) or a standard brokerage account.

**7% is a reasonable average yearly interest rate for something like a total stock market index fund, based on historical data, but in reality you will expect to see some years with higher returns and other years with lower returns.